It reminds us of the time(s) home owner insurers dropped residents of Florida after multiple hurricanes. Insurance companies are trying to stay afloat after a huge increase in claims. The soaring cost of breach incidents are changing the way insurers do business. As a result, it’s changing the way YOU do business. Insurers are requiring more from businesses before offering them cyber liability insurance coverage. And the cost of cyber liability insurance is increasing dramatically.

Have you tried to renew your cyber liability insurance? One thing you’ve noticed is the cost. The insurance premiums are higher – we’ve seen rates jump from $25,000 to $150,000. The deductibles are higher – we’ve seen $15,000 deductibles turn into $250,000.

Insurance companies are trying to cut their losses. Breaches are happening at alarming rates. Any company is a target, not matter the size.

Visit Part 3/4

Top 6 Reasons Why Your Cyber Insurer May Deny Your Claim

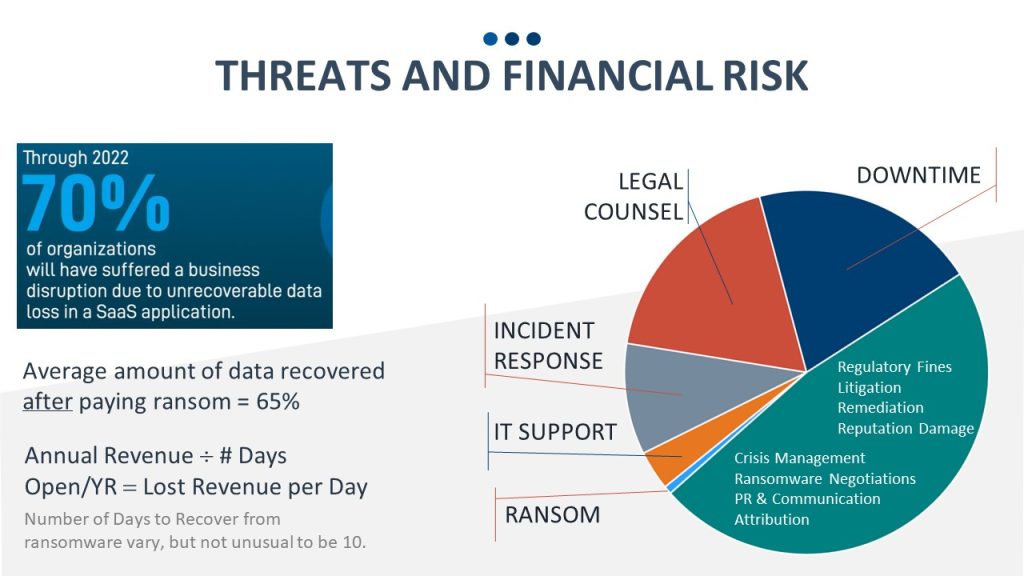

The average cost of a cybersecurity incident, such as business email compromise, data breaches and ransomware, soared from $25,000 to $100,000 from 2016 – 2021. The cost continue to rise. The total cost of Business Email Compromise in America exceeds $2.3 million.

There are many costs involved in recovering from a ransomware attack. Downtime is a costly aspect of ransomware. In the 4th quarter of 2020, the average business experienced about 21 days of downtime*, 2 days more than in the previous quarter.

Just to get a quote, insurance providers want your business to fill out lengthy questionnaires. We’ve helped our clients complete ones that have 178 questions!! Insurers want to know much more about your company’s policies, procedures and breach protection.

The top things they are looking for are also the top things that protect your business from an attack.

✅ Security Awareness Training

✅ MFA for Admin and Remote Access

✅ Encryption of Data at Rest and in Transit

✅ Inventory of Sensitive Data and Locations

✅ Disaster Recovery Testing (having a secure, recoverable backup of business-critical data)

✅ Incident Response Plan

✅ Security Event Monitoring

✅ Supply Chain Risk Management

Implement the items on the above list. Yes, there are costs to protecting your business, but it will help get you a lower cost insurance policy, avoid the costs related to a data breach and helps you avoid an insurance claim, which might price you our of future coverage.

The larger your digital footprint, the more vulnerability. Get rid of old legacy systems that have been retained just in case they are needed, consolidate old distributed network switches into switch stacks based on current technology that allows for increased performance and security, remove unused computer and user accounts, not just disable them forever.

If you have old or outdated hardware, remove or update.

Not only teach your employees about Incident Response, but have them practice. The faster you respond to issues, the less sever the damage.

You are not the only one needing to stay up to date. Your IT Partner is expected to know how to stay 1-step ahead of the threats and demands of doing business today.

If you need to escalate your IT needs, we can help. The AME Group hold certifications and undergoes routine audits to keep our business and our client’s businesses secure.

We can help you adopt a Compliance-First Mindset. Set your business up to withstand the threats and make sure you are compliant with your insurance requirements. If you do have an incident, you want to make sure your investment in your insurance will cover your costs.